By Dr. Michel Léonard, Chief Economist and Data Scientist,and Riley Conlon, Research Analyst, Triple-I

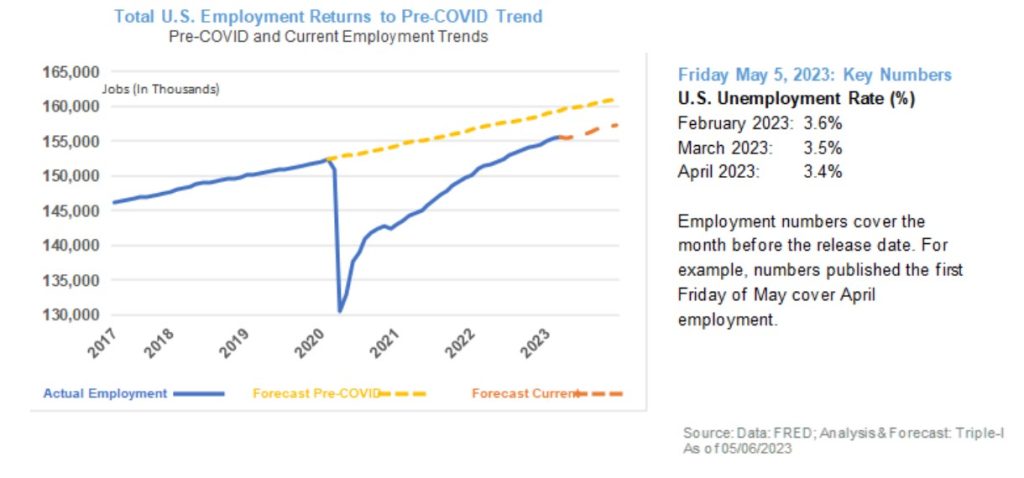

U.S. employment remains more resilient than expected given monetary tightening, adding 253,000 jobs in April, and pushing the unemployment down to 3.4 percent in April compared to 3.5 percent in March.

Jobs growth has been positive for the last 26 months, with the U.S. economy now having replaced most of the jobs lost at the beginning of the pandemic. Employment for the Insurance Carriers and Related Activities subsector specifically continues to outperform wider U.S. employment. The unemployment rate for the insurance industry was 1.6 percent in April, up from 1.5 percent in March.

Employment’s resilience and the historically low current unemployment rate are likely to add to pressure from inflation hawks on the Fed to not only continue increasing rates but to make each rate hike bigger. Based on Triple-I’s model, the spread between actual employment and the pre-COVID forward trend, which has been narrowing since the end of the pandemic, is likely to stabilize at its current level.

Aligned with this forecast and our conversations with policy makers, our view is that it is unlikely that the stronger-than-expected April jobs performance will lead the Fed to aggressively accelerate the pace of current monetary tightening; it may, however, expand the duration of the current tightening cycle.

U.S. employment has been steadily heading back to its pre-COVID growth trend. This shows great resilience, given monetary tightening. Expect the Fed to continue with “Slow and steady wins the race,” even though calls for “Monetary shock and awe” will likely grow stronger.

The legislation – signed into law by Gov. Eric Holcomb on April 20 – requires that each party in a civil proceeding and each insurer that has a duty to defend a party in court be notified of any litigation funding agreement before the case begins.

The U.S. Government Accountability Office defines third-party litigation funding as “an arrangement in which a funder who is not a party to the lawsuit agrees to help fund it.” Global multi-billion-dollar investing firms have made third-party litigation funding their sole or primary business and are experiencing strong growth.

As the market lacks transparency, estimates on its size can vary but, according to Swiss Re, more than half of the $17 billion invested into litigation funding globally in 2020 was deployed in the United States. Swiss Re estimates the market will be as big as $30 billion by 2028. Meanwhile, affordability of insurance coverage – especially for commercial auto products – has come under threat from increases in litigation and claim costs.

Several states have preceded Indiana in seeking to increase transparency around third-party litigation funding. In 2018, New York enacted legislation that added Section 489 to the New York Judiciary Law. This law mandates the disclosure of litigation financing agreements in class action lawsuits and certain aggregate settlement cases. In the same year, Wisconsin instituted a statutory provision requiring the disclosure of litigation funding arrangements. West Virginia followed suit in 2019.

In 2021, the U.S. District Court for the District of New Jersey amended its rules to require disclosures about third-party litigation funding in cases before the court. The Northern District of California imposed a similar rule in 2017 for class, mass, and collective actions throughout the district.

In 2022, Illinois passed the Consumer Legal Funding Act (S.B. 1099), which implemented several statutory provisions regulating aspects of third-party litigation funding, but it doesn’t address disclosure of these arrangements or information about the existence of a funding arrangement to defendants as part of claim litigation.

Litigation funding not only drives up costs – it introduces motives beyond achieving just results to the judicial process. This is why the practice was once widely prohibited in the United States. As these bans have been eroded in recent decades, litigation funding has grown, spread, and morphed into forms that can cost plaintiffs more in interest than they might otherwise gain in a settlement. In fact, it can encourage lengthier litigation to the detriment of all involved – except for the funders and the plaintiff attorneys.Top of Form

“Litigation funding is a multi-billion-dollar industry that for years has driven up the length and cost of civil cases,” said Neil Alldredge, president and chief executive officer of NAMIC. “While there is much more that needs to be done to address this issue, this law represents important progress.”

Revealing litigation funding from a third party before commencement of a lawsuit “will help thwart opportunistic investors from promoting return on investment over client interests and siphoning value from clients away from policyholders, claimants and insurers,” Alldredge said.

The Louisiana property insurance market has been deteriorating since the state was hit by a record level of hurricane activity during the 2020/2021 seasons, Triple-I says in a new Issues Brief on the state’s insurance crisis. Twelve insurers that write homeowners coverage in Louisiana were declared insolvent between July 2021 and February 2023.

“While similarities exist between the situations in these two hurricane-prone states, the underlying causes of their insurance woes are different in important ways,” said Mark Friedlander, Triple-I’s director of corporate communications. “Florida’s problems are largely rooted in decades of litigation abuse and fraud, whereas Louisiana’s troubles have had more to do with insurers being undercapitalized and not having enough reinsurance to withstand the claims incurred during the record-setting hurricane seasons of 2020 and 2021.”

Insurers have paid out more than $23 billion in insured losses from over 800,000 claims filed from the two years of heavy hurricane activity. The largest property loss events were Hurricane Laura (2020) and Hurricane Ida (2021). The growing volume of losses also drove a dozen insurers to voluntarily withdraw from the market and more than 50 to stop writing new business in hurricane-prone parishes.

This is not to say legal system abuse is absent as a factor in the Louisiana’s crisis – quite the opposite, as highlighted by Insurance Commissioner Jim Donelon’s cease-and-desist order, issued in February, against a Houston-based law firm. According to Donelon, the firm filed more than 1,500 hurricane claim lawsuits in Louisiana over the span of three months last year.

“The size and scope of McClenny, Moseley & Associates’ illegal insurance scheme is like nothing I’ve seen before,” Donelon said. “It’s rare for the department to issue regulatory actions against entities we don’t regulate, but in this case, the order is necessary to protect policyholders from the firm’s fraudulent insurance activity.”

McClenny Moseley has since been suspended from practice in Louisiana’s Western District federal court over its work on Hurricane Laura insurance cases.

A regular on the American Tort Reform Foundation’s “Judicial Hellholes” list, Louisiana’s “onerous bad faith laws contribute significantly to inflated claims payments and awards,” according to a joint paper published by the American Property Casualty Insurance Association (APCIA), the Reinsurance Association of America (RAA), and the Association of Bermuda Insurers and Reinsurers (ABIR).

“Insurers who fail to pay claims or make a written offer to settle within 30 days of proof of loss may face penalties of up to 50 percent of the amount due, even for purely technical violations,” the paper notes. “To avoid incurring these massive penalties, which are meted out pursuant to highly subjective standards of conduct, insurers sometimes feel compelled to pay more than the actual value of claims as the lesser of two evils.”

As a result of these converging contributors, Louisiana Citizens Property Insurance Corp. – the state-run insurer of last resort – has grown from 35,000 to 128,000 policyholders over the past two years, according to the Louisiana Department of Insurance.

At the end of 2022, the U.S. Government Accountability Office (GAO) released a report, Third-Party Litigation Financing: Market Characteristics, Data and Trends. Defining third-party litigation financing or funding (TPLF) as “an arrangement in which a funder who is not a party to the lawsuit agrees to help fund it,” the investigative arm of Congress looked at the global multibillion-dollar industry, which is raising concerns among insurers and some lawmakers.

The GAO findings summarize emerging trends, challenges for market participants, and the regulatory landscape, primarily focusing on the years between 2017 and 2021.

Why a regulatory lens on TPLF is important

The agency conducted this research to study gaps in public information about the industry’s practices and examine transparency and disclosure concerns. Three Republican Congress members – Sen. Chuck Grassley (IA), Rep. Andy Barr (KY), and Rep. Darrell Issa (CA) — led the call for this undertaking.

However, as GAO exists to serve the entire Congress, it is expected to be independent and nonpartisan in its work. While insurers, TPLF insiders, and other stakeholders, including Triple-I, have researched the industry (to the extent that research on such a secretive industry is possible), the legislative-based agency is well positioned to apply a regulatory perspective.

Example of Third-Party Litigation Financing for Plaintiffs

The report methodology involved several components, many of which other researchers have applied, such as analysis of publicly available industry data, reviews of existing scholarship, legislation, and court rules. GAO probed further by convening a roundtable of 12 experts “selected to represent a mix of reviews and professional fields, among other factors,” and interviewing litigation funders and industry stakeholders. Nonetheless, like researchers before them, GAO faced a lack of public data on the industry.

Third-party litigation funding practices differ between the consumer and the commercial markets. Comparatively smaller loan amounts are at play for consumer cases. The types of clients, use of funds, and financial arrangements can also vary, even within each market.

While most published discussions of TPLF center on TPLF going to plaintiffs, as this appears from public data to be the norm, GAO findings indicate: 1) funders may finance defendants in certain scenarios and 2) lawyers may use TPLF to support their work for defense and plaintiff clients.

How the lack of transparency in TPLF can create risks

Overall, TPLF is categorized as a non-recourse loan because if the funded party loses the lawsuit or does not receive a monetary settlement, the loan does not have to be repaid. If the financed party wins the case or receives a monetary settlement, the profit comes from a relatively high interest payment or some agreed value above the original loan. Thus, the financial strategy boils down to someone gambling on the outcome of a claim or lawsuit with the expressed intention of making a hefty profit.

In some deals, these returns can soar as high as 220%–depending on the financial arrangements–with most reporting placing the average rates at 25-30 percent (versus average S&P 500 return since 1957 of 10.15 percent). The New Times documented that the TPLF industry is reaping as much as 33 percent from some of the most vulnerable in society, wrongly imprisoned people.

Usually, this speculative investor has no relationship to the civil litigation and, therefore, would not otherwise be involved with the case. However, the court and the opposing party of the lawsuit are typically unaware of the investment or even the existence of such an arrangement. On the other hand, as the GAO report affirms, knowledge about the defendant’s insurance may be one of the primary reasons third-party financers decide to invest in the lawsuit. This imbalance in communication and the overall lack of transparency spark worries for TPLF critics. GAO gathered information that highlighted some potential concerns.

Funded claimants may hold out for larger settlements simply because the funders’ fee (usually the loan repayment, plus high interest) erodes the claimant’s share of the settlement. Attorneys receiving TPLF may be more willing to draw out litigation further than they would have – perhaps in dedication to a weak cause or a desire to try out novel legal tactics – if they had to carry their own expenses.

Regardless, typically neither the court, the defendant, nor the defendant’s insurer would be aware of the factors behind such costly delays, so they would be unable to respond proactively. However, insurance consumers would ultimately pay the price via higher rates or no access to affordable insurance if an insurer leaves the local market.

As the report acknowledges, a lack of transparency can lead to other issues, too. If the court does not know about a TPLF arrangement, potential conflicts of interest cannot be flagged and monitored. Some critics calling for transparency have cited potential national security risks, such as the possibility of funders backed by foreign governments using the funding relationship to strategically impact litigation outcomes or co-opting the discovery process for access to intellectual property information that would otherwise be best kept away from their eyes for national security reasons.

Calls for TPLF Legislation

GAO findings from its comparative review of international markets reveal that the industry operates globally, essentially without much regulation. The report points out that while TPLF is not specifically regulated under U.S. federal law, some aspects of the industry and funder operations may fall under the purview of the SEC, particularly if funders have registered securities on a national securities exchange. Some states have passed laws regulating interest charged to consumers, and, in rarer instances, requiring a level of TPLF disclosure in prescribed circumstances.

Active, visible calls from elected officials for regulatory actions toward transparency come mostly from Republicans, but, nonetheless, from various levels of government. Sen. Grassley and Rep. Issa have tried to introduce legislation, The Litigation Funding Transparency Act of 2021, requiring mandatory disclosure of funding agreements in federal class action lawsuits and in federal multidistrict litigation proceedings. In December of 2022, Georgia Attorney General Chris Carr spearheaded a coalition of 14 state attorney generals that issued a written call to action to the Department of Justice and Attorney General Merrick Garland.

“By funding lawsuits that target specific sectors or businesses, foreign adversaries could weaponize our courts to effectively undermine our nation’s interests,” Carr said.

Louisiana Insurance Commissioner Jim Donelon last week issued a cease-and-desist order against a Houston-based law firm, accusing it of fraud involving potentially hundreds of hurricane-related claims in his state.

“The size and scope of McClenny, Moseley & Associates’ illegal insurance scheme is like nothing I’ve seen before,” Donelon said in a press release. “It’s rare for the department to issue regulatory actions against entities we don’t regulate, but in this case, the order is necessary to protect policyholders from the firm’s fraudulent insurance activity.”

According to Donelon, the law firm filed more than 1,500 hurricane claim lawsuits in Louisiana over the span of three months last year.

The Louisiana property insurance market has been deteriorating since the state was hit by record hurricane activity in 2020 and 2021, to the extent that 11 insurers that write homeowners coverage in Louisiana were declared insolvent between July 2021 and September 2022. Insurers have paid out more than $23 billion in insured losses from over 800,000 claims filed from the two years of heavy hurricane activity. The largest property-loss events were Hurricane Laura (2020) and Hurricane Ida (2021).

In addition to driving insurer insolvencies, the growing losses have caused a dozen insurers to withdraw from the market and more than 50 to stop writing new business in hurricane-prone parishes.

Louisiana’s troubles parallel those of another coastal state, Florida, but there are significant differences. Florida’s problems are largely rooted in decades of legal system abuse and fraud, whereas Louisiana’s have had more to do with insurers being undercapitalized and not having enough reinsurance coverage to withstand the claims incurred during the record-setting hurricane seasons of 2020 and 2021. In general, Louisiana insurers have not experienced the level of excessive litigation that Florida insurers have faced.

“It now appears some trial attorneys are trying to take a page out of the Florida playbook by engaging in litigation abuse against Louisiana property insurers,” said Triple-I Director of Corporate Communications Mark Friedlander. “We commend Commissioner Donelon for quickly addressing these fraudulent practices.”

According to reporting by the Times Picayune/New Orleans Advocate, an investigation by the Louisiana Department of Insurance found the Houston-based firm engaged in insurance fraud and unfair trade practices through Alabama-based Apex Roofing and Restoration and has faced accusations of potentially criminal behavior in courts across the state. In one such case, the paper reported, a woman testified that she had never intended to retain the law firm when she hired the roofing company to fix her hurricane-damaged roof.

“The firm told her insurance company that it represented her and even filed a lawsuit on her behalf, though she said she was unaware of it,” the paper said.

Legal system abuse is a pervasive problem that contributes to higher costs for insurers and policyholders nationwide, as well as to rising costs generally, given the importance of insurance in development and commerce. Triple-I is committed to informing the discussion around this critical issue.

Florida Gov. Ron DeSantis’s proposed insurance fraud and legal system abuse reforms, announced this week for consideration during the legislative session that begins in March, would build on measures approved in the closing weeks of 2022 and go a long way toward fixing the state’s insurance crisis.

Legislation passed during the 2022 special session eliminated one-way attorney fees and assignment of benefits (AOB) arrangements for property insurance claims. Gov. DeSantis’s proposal would go further, eliminating these mechanisms and “attorney fee multipliers” for all lines of insurance.

“For decades, Florida has been considered a judicial hellhole due to excessive litigation and a legal system that benefitted the lawyers more than people who are injured,” DeSantis said in his announcement. “We are now working on legal reform that is more in line with the rest of the country and that will bring more businesses and jobs to Florida.”

Before the 2022 reforms, state law required insurers to pay the fees of homeowners insurance policyholders who successfully sued over claims, while shielding policyholders from paying insurers’ attorney fees when the policyholders lose. The legislation also eliminated AOBs – agreements in which property owners sign over their claims to contractors, who then work with insurers.

AOBs are a standard practice in insurance, but in Florida this consumer-friendly convenience has long served as a magnet for fraud. The state’s legal environment – including some of the most generous attorney-fee mechanisms in the country – has encouraged vendors and their attorneys to solicit unwarranted AOBs from tens of thousands of Floridians, conduct unnecessary or unnecessarily expensive work, then sue insurers that deny or dispute the claims.

As a result, Florida accounts for nearly 80 percent of the nation’s homeowners’ insurance lawsuits, but only 9 percent of claims, according to the state’s Office of Insurance Regulation.

Eliminating these two mechanisms for property claims addresses much of the insurance fraud in the state. Eliminating them for all lines would be a promising sign that the state is truly committed to addressing the root causes of the crisis.

Florida’s insurance crisis didn’t happen overnight, and it will take years for the impacts of fraud and legal system abuse to be wrung out of the system. Policyholders won’t see premium benefits any time soon. Job 1 is to “stop the bleeding” as insurers fail, leave the state, or stop writing critical personal lines coverages like auto and homeowners.

Triple-I has published a new Issues Brief about the crisis and the state’s efforts to repair it.

Legislation being considered in Illinois underscores the need for legislators and other policymakers to become better educated about the importance of risk-based pricing and how it works.

The Motor Vehicle Insurance Fairness Act would bar insurers from considering nondriving factors, such as credit scores, when setting premium rates. The prohibitions include factors that actuaries have demonstrated correlate strongly with the likelihood of a driver eventually submitting a claim, as well as ones insurers already are prohibited from using.

This suggests a lack of understanding about risk-based pricing that is not isolated to Illinois legislators – indeed, similar proposals are submitted from time to time at state and federal levels.

Confusion is understandable

Risk-based pricing means offering different prices for the same coverage, based on risk factors specific to the insured person or property. If policies were not priced this way, lower-risk drivers would subsidize riskier ones. Charging higher premiums to higher-risk policyholders helps insurers underwrite a wider range of coverages, improving both availability and affordability of insurance.

The concept becomes complicated when actuarially sound rating factors intersect with other attributes in ways that can be perceived as unfairly discriminatory. For example, concerns are raised about the use of credit-based insurance scores, geography, home ownership, and motor vehicle records in setting home and car insurance premium rates. Critics say this can lead to “proxy discrimination,” with people of color in urban neighborhoods being charged more than their suburban neighbors for the same coverage.

Confusion is understandable, given the complex models used to assess and price risk. To navigate this complexity, insurers hire actuaries and data scientists to quantify and differentiate among a range of risk variables while avoiding unfair discrimination.

Appropriate protections are in place

It’s important to remember that insurers don’t make money by notinsuring people. They are in the business of pricing, underwriting, and assuming risk.

Because of the critical role insurers play in facilitating commerce and protecting the lives and property of individuals, insurance is one of the most heavily regulated industries on the planet. To ensure that sufficient funds are available to pay claims, regulators require insurers to maintain a cushion called policyholder surplus.

Credit rating agencies, such as Standard & Poor’s and A.M. Best, expect insurers to have surpluses exceeding what regulators require to keep their financial strength ratings. A strong financial strength rating enables insurers to borrow money at favorable rates – further promoting insurance availability and affordability.

On top of these constraints, state regulators have the authority to limit the rates insurers can charge within their jurisdictions.

No profit, no insurers — no insurers, no coverage

Like any other business, insurers must make a reasonable profit to remain solvent. Because they can’t just move money around as more lightly regulated industries can, the only way to generate underwriting profits is through rigorous pricing and expense and loss controls. Insurers don’t want to overcharge and send consumers shopping for a better price, or undercharge and experience losses that erode their ability to pay claims.

In this context, it’s important to note that personal auto and homeowners insurance premium rates have remained relatively flat as inflation and replacement costs have soared through the pandemic and supply-chain issues related to Russia’s invasion of Ukraine (see chart below).

During this period, writers of these coverages have struggled to turn an underwriting profit. Personal auto has been a primary driver of the overall industry’s weak underwriting results. Dale Porfilio, Triple-I’s chief insurance officer, recently said the 2022 net combined ratio for personal auto insurance is forecast at 111.8, 10.4 points worse than 2021 and 19.3 points worse than 2020. Combined ratio represents the difference between claims and expenses paid and premiums collected by insurers. A combined ratio below 100 represents an underwriting profit, and one above 100 represents a loss.

Even as inflation moderates, loss trends in both of these lines – associated with increased accident frequency and severity in auto and extreme-weather trends in homeowners and auto – will require premium rates to rise. The question is: Will the cost fall evenly across all policyholders, or will rates more accurately reflect policyholders’ risk characteristics?

Protected classes

The United States recognizes “protected classes” – groups who share common characteristics and for whom federal or state laws prohibit discrimination based on those traits. Race, religion, and national origin are most commonly meant when describing protected classes in the context of insurance rating, and insurers generally do not collect information on these “big three” classes. Any discrimination based on these attributes would have to arise from using data that might serve as proxies for protected classes.

Algorithms and machine learning hold great promise for ensuring equitable pricing, but research shows these tools can amplify implicit biases.

The insurance industry has been responsive to such concerns. For example, recent Colorado legislation requires insurers to show that their use of external data and complex algorithms does not discriminate against protected classes, and the American Academy of Actuaries has offered extensive guidance to the state’s insurance commissioner on implementation. The Casualty Actuarial Society also recently published a series of papers (see links at end of post) on the topic.

Correlation matters

Certain demographic factors have been shown to correlate with increased risk of submitting a claim. Gender and age correlate strongly with crash involvement, as the National Highway Traffic Safety Administration (NHTSA) data illustrated at right shows.

Likewise, National Association of Insurance Commissioners (NAIC) data below clearly shows higher credit scores correlate strongly with lower crash claims.

Similar correlations can be shown for other rating factors. It’s important to remember that no single factor is determinative – many are used to assess a policyholder’s risk level.

Consumers “get it” – when it’s explained to them

A recent study by the Insurance Research Council (IRC) found consumer skepticism about the connection between credit history and future insurance claims appears to decline when the predictive power of credit-based insurance scores is explained to them. Through an online survey with more than 7,000 respondents, IRC found that:

Nearly all believe it is important to maintain good credit history, and most believe it would be “very” or “somewhat” easy to improve their credit score;

Consumers see the link between credit history and future bill paying but are less confident about the link between credit history and future insurance claims.

After reading that many studies have demonstrated its predictive power, most agree with using credit-based insurance scores to rate insurance, especially for drivers with good credit who could benefit.

If consumers “get it” when you share the data with them, perhaps policymakers and legislators can, too.

Triple-I fields a lot of questions from consumers and the media as to exactly how inflation affects insurance premium rates. As we explain in a new Issues Brief, the relationship between inflation and rates is, in one sense, straightforward – and yet the outcomes are not necessarily what you might expect.

As material and labor costs rise, the cost to repair and replace damaged homes and vehicles increases. If premium rates didn’t reflect these increased costs, insurers would quickly exhaust the funds they set aside – “policyholder surplus” – to ensure that they can afford to keep their promises to pay all claims. If losses and expenses exceed revenues by too much for too long, they risk insolvency.

But insurers do more than pay claims: They employ people (labor costs) and conduct business operations (supplies and energy costs); and, if they are to remain in business, they have to earn a reasonable profit.

So, when inflation and replacement costs rise, one might reasonably expect a proportionate increase in auto and homeowners insurance premium rates. But, as the charts below show, rates remained relatively flat during 2021’s sharply higher costs that coincided with the height of the COVID-19 pandemic.

In addition to not increasing rates proportionately to rising costs, personal auto insurers – expecting reduced losses as fewer drivers were on the road during lockdown – returned about $14 billion to policyholders through cash refunds and account credits. While loss ratios fell briefly and sharply in 2020, they have since climbed steadily to exceed pre-pandemic levels.

With drivers fully on the road again, this loss trend is expected to continue.

It’s important to remember that the decreases in CPI and replacement costs indicated above do not represent cost declines but, rather, reduced rates of growth. These and other forces – such as unfavorable accident fatality trends and population shifts into disaster-prone regions – will continue to apply upward pressure on premium rates.

Moderating inflation and replacement costs provide glimmers of hope for property & casualty insurers, but underwriting profitability will remain a challenge for most lines of business for the foreseeable future, according to actuaries at Triple-I and Milliman, a risk-management, benefits, and technology firm. Their findings were presented at a Triple-I’s quarterly members-only webinar.

Dr. Michel Léonard, Triple-I chief economist and data scientist, forecast that costs of materials and labor involved in replacing or repairing insured property will decline from 8.1 percent at year-end 2022 to 4.5-6.5 percent at the end of 2023 on the way to 0.9 percent in 2024. Supply-chain issues since the start of the COVID-19 pandemic and Russia’s invasion of Ukraine have kept replacement costs at historic highs.

When the cost to repair or replace damaged cars or homes is high, premium rates that determine how much policyholders pay for coverage should rise proportionately. As Triple-I has previously reported, though, this has not been the case for homeowners and auto insurance. Premium rates for both of these lines of insurance have not kept up with rising costs. As a result of these and other factors, insurers have struggled to remain profitable.

Personal auto replacement costs, Dr. Léonard projected, will fall from nearly 10 percent to near 0 percent by 2024. Homeowners replacement costs are predicted to fall from 7.6 percent to below 2 percent by 2024.

Worsening profitability generally

The P&C industry’s 2022 combined ratio – a measure of underwriting profitability – is estimated at 105.8, a 6.3-point worsening from 2021. Combined ratio represents the difference between claims and expenses paid and premiums collected by insurers. A combined ratio below 100 represents an underwriting profit, and one above 100 represents a loss.

For the overall P&C industry underwriting projections, Porfilio said, “We forecast premium growth of 8.4 percent in 2022 and 8.5 percent in 2023, primarily due to hard market conditions and exposure growth.”

The personal auto line of insurance has been a primary driver of the industry’s weak underwriting results. Dale Porfilio, Triple-I’s chief insurance officer, said the 2022 net combined ratio for personal auto insurance is forecast at 111.8, 10.4 points worse than 2021 and 19.3 points worse than 2020. He said supply-chain disruption, labor shortages, and costlier replacement parts all contribute to current and future loss pressures.

For the commercial multi-peril line, Jason B. Kurtz, a principal and consulting actuary at Milliman, said underwriting losses are expected to continue.

“Insurers will need to consider rate increases to offset economic and social inflation loss pressures,” Kurtz said.

Dave Moore, president of Moore Actuarial Consulting, said the 2022 combined ratio for commercial auto is forecast to have worsened in 2022. Moore also stated that general liability is deteriorating.

“We forecast a small underwriting profit for 2023 and 2024, but inflation and geopolitical risk put pressure on these forecasts,” he said, adding, “premium growth from the hard market is forecast to slow in 2022 to 2024.”

For the commercial property line, Kurtz noted that the industry is seeing strong premium growth and that rate increases should help alleviate some of the pressure from catastrophe losses. Despite Hurricane Ian, he said he expects an underwriting profit in 2022, continuing into 2023 and 2024.

Donna Glenn, chief actuary at the National Council on Compensation Insurance, noted that the workers compensation line of business has seen declines in rates and loss costs for several years, partially driven by reductions in on-the-job accident frequency. This line, Glenn added, is expected to continue its profitability.

Inflation, interest rates, and recession will dominate the U.S. economic narrative in the first quarter of 2023, shifting in the second and third to a focus on timing of recovery and a more neutral monetary policy and, in the fourth, whether and when the Fed will signal the start of a new easing cycle, according to Triple-I Chief Economist and Data Scientist Dr. Michel Léonard.

“We forecast the U.S. economy to grow 3.2 percent in 2023, up from 2.6 percent in 2022,” Léonard says. The U.S. Consumer Price Index (CPI) ended 2023 at 6.5 percent year over year, down from a high of 9.1 percent year over year in June. “Triple-I expects inflation to continue to decline throughout 2023, though not equally from one to the next quarter. The pace and extent of any inflation slowdown are predicated on improvements in global geopolitical risk.”

P&C underlying growth, which has been below overall GDP since the start of the pandemic, is likely to grow at a faster pace than the rest of the U.S. economy throughout the year.

“We remain cautious and forecast insurance underlying growth for 2023 to be around 3 percent, up from 2 percent in 2022,” Léonard says. “We forecast P&C replacement costs to increase by between 4.5 percent and 6.5 percent year-over-year in 2023. P&C replacement costs increased on average 25 percent since the beginning of the COVID-19 pandemic in 2020.”

Even though Triple-I expects economic fundamentals to improve throughout 2023, line-specific underwriting considerations will continue to depress performance, Léonard says.

Triple-I members can access the Triple-I’s Economic Dashboard, available at the organization’s members-only website. The Dashboard’s ongoing updates allow insurance industry professionals to follow key economic reports (e.g., federal governmental updates on interest rate, unemployment, and housing trends) in real time, adjust forecasts, and recalibrate strategy. Each quarter, the Triple-I’s Outlook provides a road map about which key economic reports will most impact insurance industry performance.

To learn about the benefits of Triple-I membership, click here.